NEW YORK — Tough times have a way of putting things in perspective for people. For young adults, financial hardships caused by COVID-19 have been a real eye-opener. A survey finds seven in 10 millennials and Gen Zers say the pandemic made them realize they needed to reset and reevaluate how they handle their money.

The new OnePoll study asked 1,000 Gen Z Americans and 1,000 American millennials about the impact of the COVID-19 pandemic and 2020 as a whole on their personal finances.

Over half (52%) said they wish they did a better job handling their money during the pandemic. In a show of generational differences, millennials are more likely than their Gen Z counterparts to feel like they handled their money poorly (59 percent to 46%).

The poll, commissioned by Laurel Road, a digital lending platform and brand of KeyBank, reveals the top reasons for a financial reset included new personal goals (33%), changes to their personal life (32%), and new financial goals (30%).

The best laid budgets of mice and men…

Although nearly seven in 10 respondents shared they’ve effectively budgeted their money as best they could, given the circumstances of 2020 and quarantine in particular, 60 percent also said they wish they could improve their budgeting skills, but they just don’t know where to begin.

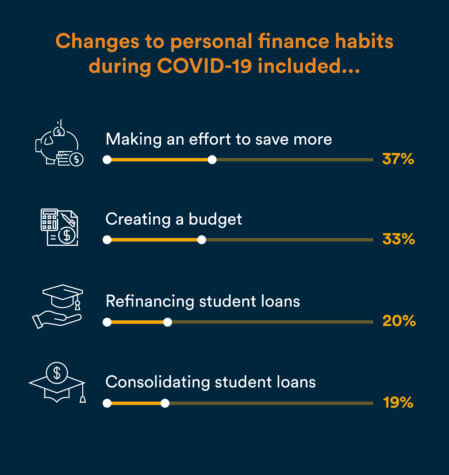

Thirty-seven percent of respondents said they made more of an effort to save more money when they could, with 33 percent creating a budget and 25 percent even speaking to a financial adviser about their situations. Another 20 percent of those polled shared they refinanced their student loans and 19 percent consolidated their student loans.

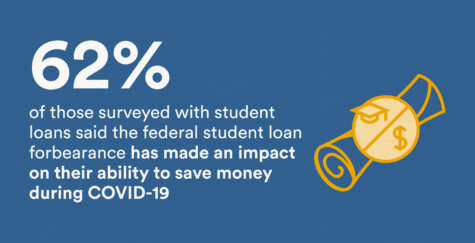

For those polled with student loans (approximately 1,500 respondents), 62 percent said the federal student loan forbearance has made an impact on their ability to save money during the pandemic.

These quick adaptations during this uncertain time seemed to have paid off, as the average Gen Z respondent saved nearly $600 and the average millennial saved just over $1,000 during the pandemic.

“We know COVID-19 has been challenging for us all. For millennials and Gen Z-ers, they too have faced many challenges, but in turn, the pandemic has also prompted an opportunity for a financial reset,” says Alyssa Schaefer, Chief Experience Officer at Laurel Road, in a statement. “What’s encouraging to see from our survey results is that so many people have used this time to prioritize their personal finance, including by refinancing their student loans, and actively look to learn new ways to budget and save.”

Millennials opening their wallets for self-improvement

Respondents also shared the top ways they’ve been investing in themselves during this uncertain time. One in three (32%) are putting money toward personal wellness and one in four are investing in their professional development by getting certified in additional skills.

Encouragingly, a quarter (25%) of respondents also shared they’ve put more money toward mental health resources as well as attending webinars or online courses to build their professional development (24%).

Student loans can play a big part in Gen Z and millennials’ financial wellness. The survey finds that 62 percent of those surveyed with student loans shared that quarantine finally allowed them the time to think about their student loan financing options.

“Investing in personal well-being is always important and something we believe in strongly at Laurel Road,” Schaefer adds. “Right now, it’s never been more crucial to focus on our ‘mental wealth’ – daily personal, professional and financial decisions that support our peace of mind. Making impactful changes to financial planning, such as student loan refinance, can create beneficial savings opportunities, and we’re proud to provide options that do this for our customers.”

Looking ahead to next year, one in five respondents shared that if they had an extra $1,000 to spend in 2021 they’d use it to pay off more of their student loans. Additionally, a quarter of respondents said they would invest in their personal wellness and even in the stock market.